http://www.zdnet.com/article/the-enterprise-technologies-to-watch-in-2016/

THE ENTERPRISE TECHNOLOGIES TO WATCH IN 2016

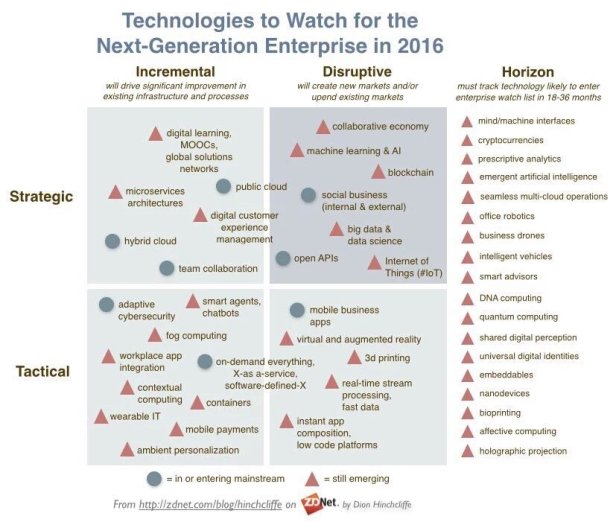

- Microservices architectures. Often argued as service-oriented architecture both done right and made practical, the approach of lightweight, modular, stateless, API-enabledmicroservices have come into their own recently, with numerous compelling examples, in particular the success of Netflix with the approach, to the point that most organizations should carefully consider the technique given the known benefits. This includes scalability, reliability, cost-effective operation, improved resiliency, an easy path to containers, and ease of deployment. Recent survey data has shown the microservices are now in production already in a third of organizations today.

- Digital learning, MOOCs, global solutions networks. Not noticed as much outside of the learning and development industry are the rapid changes that digital technology is having on human learning. Improving learning enables both the fuller realization of workforce potential and is also the path to becoming and staying a digital leader, as maintaining effective digital skills in the pace of very rapid technological progress is perhaps our greatest challenge today, and is why education technologies have remained on the list. From digital learning tools for the individual such adaptive learning, for which students are reporting very positive responses, to massive open online courses (MOOC), to global solutions networks so entire industries can learn from each other, remain the top learning technologies in 2016 as I explored in my vital digital trends list last year. Rapid growth is particularly evident in the MOOC industry, which is currently growing exponentially and recently reached 4.55K total available online courses.

- Public cloud. Few enterprises have shifted entirely to public cloud yet, but that increasingly appears to be the ultimate end state when looked at over a timescale longer than 18-36 months. While private and hybrid cloud are considered ‘starter cloud’ models for most organizations, recent data show that public cloud will ultimately dominate. While still having the smallest level of adoption compared to private and hybrid, public cloud has a highest rate of growth, at a ferocious average annual compound annual rate of 44% through 2019. Public cloud will now overtake private cloud in usage between 2017 and 2018. Probably the latest significant shift in the public cloud landscape is that Microsoft Azure is finally making real — though still early — gains against against uber-dominant market leader’s Amazon Web Services’s impressively full spectrum of cloud offerings.

- Digital, customer experience management (DX, CEM). Creating a consistent, well-organized, and effective user experience across all digital channels — from mobile appsto strategic online communities — is one of the hotter topics in digital experience these days. As I explored recently, actually achieving a truly integrated digital experience is a tall order, but one that is worth real investment, as it can pay very substantial benefits: Customer experience leaders significantly outperform the S&P 500. The customer experience management market is currently expected to grow at an annual rate of 19.9%from 2015 to 2020.

- Team collaboration. The poster child in the revitalization of this space continues to be the success story of Slack, a real-time messaging application that has blazed a unique trail and discovered a new model for effective team-based collaboration, one that is extremely lightweight, channel organized, and connects with a large number of 3rd party applications to create a singular, personalized, and impactful collaboration experience. While enterprise social networks, the leading new model for collaboration before now, still excel at mass collaboration at the organization and departmental level, I suggested earlier this year that most organizations must prepare for a multi-layered collaborationapproach that incorporates these new lightweight tools. The big enterprise vendors are responding in kind or with other innovative approaches. Notable examples include Project Toscana from IBM, Microsoft’s new Gigjam, and even Google’s new Spaces.

- Hybrid cloud. For many an important interim step, hybrid cloud allows moving workloads out to the public cloud when it makes sense for reasons of cost, control, scalability, and security. While I believe that enterprises should not wait to learn about the full set of issues they will encounter in moving to public cloud — and the best way to do that is to try to get there as quickly and completely as possible — hybrid cloud is the second best options. Most organizations should be seriously investing in hybrid cloud in 2016 if they are not ready for a more direct move to public cloud. Hybrid is also the most popular cloud option according to the latest available data, with 18% and 6% doing public-only and private-only cloud respectively, and 71% of organizations survey having instead a hybrid cloud infrastructure currently.

- Social business (internal and external.) The journey of creating more networked and collaborative organizations with our customers, partners, and employees by employing social tools remains a major and still unfolding trend that many organizations are currently grappling with. The latest data shows that social business remains a fast-growth industry. Probably the most thorough view currently on how the practice and technologies are reshaping organizations is in McKinsey’s just-released a broad based new examination of the results organizations are achieving with social business. Research firm Technavio reported earlier this year that social business investment will have an annual compound growth rate of 26% through 2019, to reach $23 billion ≈ cost of 2004 Hurricane Ivan

≈ Harry Potter movie franchise revenue≈ cost of 2005 Hurricane Wilma≈ cost of construction of Channel tunnel connecting the UK to France≈ Manhattan Project, the original US program to develop the atomic bomb

“>[≈ net worth of Charles Koch, American business man, 2011].

- Machine learning and artificial intelligence. If the amount of venture investment taking place in an industry is indicative of future growth, machines that might actually be able to think for themselves in the name of solving hard business problems is on a hot streak. Elon Musk himself recently invested in the OpenAI initiative, which is a $1 billion ≈ box office sales of The Jungle Book, 1967

≈ box office sales of ET: The Extra-Terrestrial, 1982≈ box office sales of The Exorcist, 1973≈ box office sales of Jaws, 1975

“>[≈ net worth of J.K. Rowling, author of the Harry Potter series, 2011] backed think tank to research the key issues and ensure that AI will be a “benefit to humanity”. Yet the revenue of the industry is currently a minuscule $202 million [≈ Mitt Romney assets in 2011] today, showing that a lot more is about to happen. This is expected change dramatically growth-wise, with artificial intelligence industry expected to bring in over $11 billion ≈ MIT university endowment in 2011

≈ cost of 2004 Hurricane Frances“>[≈ cost of 1989 Hurricane Hugo] by 2024.

- Collaborative economy. Also known as the sharing economy, startups like Uber and Airbnb showed showed definitively that peer sharing as a business model based in the real-world yet deeply enabled by digital technology, not only had legs but could permanently displace market leaders that used more traditional methods of value creation. While leading thinkers in the space such as Jeremiah Owyang have noted that in 2016 we’re now in the early maturity phase of the collaborative economy, the collective growth has barely begun. The fundamental reason every company must now consider the opportunities and threats that these transformational business models bring to the table? The economics: The total size of the market is anticipated to be vast, withPwC pegging it at $335 billion ≈ US annual charitable giving, 2010

≈ cost of World War I≈ US corporate research and development, 2010≈ US Medicaid spending, 2005≈ All US higher education spending, 2002

“>[≈ cost of US-Korean War] by 2025

. - Blockchain. Few other technology advances have emerged recently that have received as much adoring analysis as blockchain, the distributed ledger technology that underpins cryptocurrencies like Bitcoin. My analysis last year made a similar finding however, and we’re now seeing traditional industries, from finance to insurance, pilot or rollout the technology to ensure a new level of trust, transparency, and security for transactions of just about any kind. What’s the growth vector for blockchain? Industry growth numbers are hard to come by, but venture investment has now surpassed $1.1 billion ≈ net worth of J.K. Rowling, author of the Harry Potter series, 2011

≈ box office sales of ET: The Extra-Terrestrial, 1982≈ box office sales of The Exorcist, 1973≈ box office sales of Jaws, 1975≈ box office sales of The Sound of Music, 1965

“>[≈ box office sales of 101 Dalmatians, 1961]

and is expected to continue. It is likely, in my opinion, that blockchain will become a major industry soon in its own right. Companies should be looking to leverage the technologies for its strengths in creating far more assurance, safety, and trustworthiness in high value business activities in the connected era. - Big data and data science. While the some of the hype is off the big data trend, the concept of processing vast amounts of data from many disparate sources — to closewhat I’ve noted has been called the “clue gap” — to derive vital insights ahead of competitors. Data-driven business functions of every type now abound, but in my experience, many organizations are still fairly early in their days of actually using the techniques strategically and truly closing open loop processes. One significant issue: Far too many organizations are awash in insights they are not structured or resourced to respond to. The expected growth of the industry tells the story of how much there is still left to do: Wikibon now expects the big data industry to hit $92 billion [≈ Federal Reserve profit in 2010] in revenue by 2026 and maintain an annual growth rate of 14.4% through that time.

- Internet of Things (IoT). Perhaps one of the most significant new industries in the technology business, the digital connectedness of everything that the Internet of Things represents has begun. My examination of the IoT industry found that the technology is truly strategic to the enterprise as a way to maintain deep levels of deep real-time perpetual engagement and data-driven enablement to customers at scale. Even though estimates put the economic opportunity at up to a whopping $14.4 trillion ≈ US GDP, 2011

≈ 2008 US GDP≈ 2009 US GDP≈ 2005 US GDP≈ 2006 US GDP≈ 2011 US GDP≈ 2007 US GDP

“>[≈ 2010 US GDP] annually by 2022

, many companies still don’t have a cogent IoT strategy to head off competitors who are looking at IoT to create a new permanent digital beachhead in their business customers around the world. - Virtual and augmented reality. A powerful combination of immersive user experience, both VR and AR have some work to do in order to get the display resolutions high enough, the form factor compact enough, and compelling solutions to market that will provide benefit to the average worker. Yet it’s clear to me that all of this is almost certainly going to be resolved and these advances are a major part of the future of user experience. Poster children include Oculus Rift, Microsoft HoloLens, and Magic Leap. AR and VR are forecast to be a combined $120 billion ≈ Cost of all cancer treatment in the United States, 2008″>[≈ cost of Hurricane Katrina] industryby 2020.

- Mobile business apps. For a variety of reasons related to new and unfamiliar platforms to enterprise IT developers, mobile device management industry flux, and the sheer churn in the hardware market, mobile business applications have developed far more slowly than consumer apps. Yet the market, by some estimates will be $56 billion ≈ net worth of Warren Buffett, 2011

≈ all real estate in Bronx, NYC, 2010

“>[≈ net worth of Bill Gates, 2011] by 2017

. Other recent data shows the potential value and overarching trends: 90% of companies will increase mobile app investment in 2016, with those with mobile workforces seeing substantial ROI. - 3D printing. The complexities and immaturity of the 3D printing industry often obscures its true promise: The ultimate ability to mass customize and conveniently produce just-in-time virtually all of the objects we need to operate our businesses. Still nascent technology, with decades more of development required, the concept of the Star Trek replicator will eventually achieve real-world fruition through the realization of this technology. The market forecast for 3D printing technology is to reach $30 billion ≈ Hong Kong international airport

≈ Harvard University endowment in 2011

“>[≈ cost of 2008 Hurricane Ike] by 2022, at a 28.5% growth rate. Ultimately, most companies making finished goods must consider how their products can be disrupted by customers producing what they need on-demand at their own facilities.

- Real-time stream processing, fast data. While big data purports to be able to process vaster amount of diverse data than ever before, real-time stream processing promises to handle Hadoop-scale continuous data streams in round-the-clock without falling behind. Whether you’re handling data streams from millions of ongoing user interactions or looking for instantaneous stock trading insights, technologies like Apache’s Spark Streaming enables scalable, fault-tolerance processing of vast streams of information. The Spark market alone will be worth $11.5 billion ≈ cost of 1972 Hurricane Agnes

≈ cost of 2005 Hurricane Rita

“>[≈ cost of 2004 Hurricane Frances] by2020 according to recent estimates.

- Instant app composition, low code platforms. Platforms like Mendix, IFTTT, and Zapiermake now it incredibly easy to automate the creation, integration and data flow of highly useful simple applications. Low code platforms, as identified by Forrester’s recent Wave report, will be a $10 billion ≈ Construction cost for Gerald R. Ford-class aircraft carrier

≈ cost of Spanish-American War≈ Chernobyl costs, USD at the time≈ MIT university endowment in 2011≈ cost of 1989 Hurricane Hugo

“>[≈ cost of 2004 Hurricane Frances] industry by 2019

. Speed of development, low cost, and disposal apps that don’t need to be maintained are key advantages that can enable far more situational applications to meet needs for IT solutions as they emerge. 62% of low code developers report completing low code solutions within 2 weeks. I’ve long believed that once successful models were hit upon, low code will unleash a generation of citizen developers, though some have argued that tools like Microsoft Excel have long enabled this. - On-demand everything, X-as-a-Service, Software defined X. The online service-enablement of IT infrastructure is one of the biggest industries in the technology business already, recently calculated to be $203 billion ≈ UN estimated cost to end world hunger, 2011

≈ cost of NASA Space shuttle program≈ cost of San Francisco 1906 earthquake≈ all real estate in Brooklyn, NYC, 2010≈ Mobile computer industry sales, 2011

“>[≈ Annual credit card fraud as of 2009]

by the end of 2016. Making everything on-demand, instantly available, and highly elastic has enormous operating and cost advantages, enabling new types of applications heretofore not possible. - Containers. Often cited as one of the key technologies to enable a robust and modern hybrid cloud, containers like Docker continue their rise in 2016 as an effective way to deconstruct monolithic application architectures in favor of lightweight microservices, ushering in far more cloud friendly enterprise architectures.

- Mobile payments. Most businesses will need to seriously consider mobile payment services like Apple Pay and Samsung Pay on their roadmaps as 1 in 5 mobile users willuse the digital payment services next year, reaching a tipping point.

- Ambient personalization. As social channels taxes traditional marketing agencies, the next big push in digital marketing and customer experience is pervasive personalization. Instant real-time provisioning right as you arrive at a site or use a Web applications. This is already happening with online ad retargeting (those ads that follow you around the Internet), but the level of sophisticated is about to go off the charts. Personalizationcurrently tops the list of digital marketing trends in 2016.

- Wearable IT. Led by the breakout entry in the market of the Apple Watch, Gartner says wearables will grow 18% in 2016 to 50 million units. While very early days in the enterprise space, the market is expected to grow dramatically as health and field enablement solutions enter the market and mature.

- Contextual computing. Too much of our IT today still requires us to create and connect the context between different applications. Why can’t our digital calendars help fill out our time sheets? What can’t our CRM system know which client we’re currently visiting and bring up the record automatically when we launch it. The next generation of productivity in the workplace will come from more contextually aware applications that would exhibit what we would otherwise call common sense.

- Workplace app integration. Popular messaging apps like Wechat and Slack have shownhow useful it is having important apps integrated in the way we communicate and collaborate. I’ll be released research soon that shows that app integration substantially increases the value of digital engagement. Having been a proponent of app integration in our social tools since the advent of OpenSocial, it now increasingly looks like the way forward has been found.

- Adaptive cybersecurity. Cybersecurity routinely makes the top 5 list of CIO concerns. Increasingly, instead of fixed solutions to security issues, artificial intelligence is being incorporated into IT security product to dynamically investigate and respond to unique and emergent security breaches on the fly. MIT recently developed an AI agent that can detect 85% of breaches.

- Smart agents, chatbots. Heralded by mobile device agents like Siri and Cortana, or smart devices like Amazon Echo, smart agents and chatbots are going to be a big part of the next wave of user interface, using voice and other high bandwidth channels, according to my analysis of the fast growing space. Dan Grover, WeChat product manager, probably provided the best detailed overview of this significant new approachin a blog post recently. Increasingly consumers will expect their businesses to offer solutions that enable highly convenient, frictionless conversational experiences.

- Fog computing. Sometimes known as the Internet of Everything, fog computingdescribes the use of a collaborative cloud of end-user clients or nearby edge devices that can contribute bandwidth, storage, and other resources on demand for higher performance and fault tolerance for demand applications, without the limitations of accessing far away cloud data centers. A continuum of the cloud computing spectrum, there’s always an OpenFog Consortium. Fog computing will enable new types of applications that aren’t possible using more narrow end-to-center cloud architectures.